Cash flow, invoices and payments

Good customer and supplier management will ensure you have a consistent flow of money coming in from sales to be able to pay your bills.

Learn how to develop invoices and manage your debtors (people who owe you money), as well as how to pay and build strong relationships with your creditors (your suppliers).

Cash flow is the movement of money in and out of your business. The money coming in is called revenue, and the money going out is your cost of operations.

Good cash flow management will ensure you always have money available to pay expenses, both expected and unexpected.

Your cash flow can be impacted if your customers (debtors) don't make their payments to you on time. In turn, you may not be able to make payments to your suppliers (creditors) or lenders. Even profitable businesses can fail if they are not managing their cash flow properly.

Watch our video to help you understand how to manage the money coming in and going out of your business.

-

Not having enough money is one of the biggest reasons small businesses fail.

Think of cash flow as the fuel that keeps your business running.

It's the money coming in and going out.

If you generate more revenue than expenses, this indicates good financial health.

For example, Lucy is the owner of a flower shop. If Lucy's revenue exceeds her expenses, she can pay her bills on time, pay her employees and herself, put money back into the business so it can grow and improve and invest in her superannuation fund.

If you are looking to improve your cash flow, you can take 4 basic steps right now to help your business thrive.

1. Track your budgeted revenue and expenses against your actual revenue and expenses. This will help you monitor your cash flow and notice any potential cash flow problems before they occur.

Use accounting software or a spreadsheet regularly to help you calculate budget forecasts and expected cash flow for future months. This will show you where you might not have enough cash to pay all your upcoming expenses.

2. Make it easy for your customers to pay you.

You can do this by invoicing customers quickly, providing clear payment terms, offering multiple payment options and monitoring upcoming invoice payments.

3. Keep on top of your expenses by securing the best rate from providers and suppliers, paying expenses on the due date, managing staff wages by rostering less staff in non-busy periods and keeping your business and personal bank accounts separate so your business costs are easy to track.

And 4. If you're a business that relies on stock, be sure to monitor and review your stock levels regularly.

Too much stock can tie up your cash or leave you with unmovable stock, and too little can impact customer demand and leave customers empty-handed.

So, to keep your cash flow moving in the right direction and fuel your business for success remember to stay on top of your monthly budget, make it easy for your customers to pay you, keep on top of your current and future expenses and monitor and review your stock.

If you need more help on managing your cash flow, talk to your accountant or financial adviser or visit the Business Queensland website.

Working capital

Working capital is the difference between your business's current assets (such as cash and accounts receivable) and your current liabilities (such as accounts payable). It is a measure of your business's short-term financial health.

The cash flow of your business is represented by your level of working capital. This is made up of 3 core components:

- managing your stock

- collecting customer payments

- making supplier and creditor payments.

If you have more current liabilities than current assets, you could have trouble growing your business or paying back creditors. It can also affect your ongoing business registrations and access to contracts or lead to bankruptcy.

The 'working capital cycle' is the length of time it takes from you using cash to purchase stock or other business inputs to receiving the cash back from a debtor or sale. Think of it as a loop, starting with cash at the top.

Identify the period between the different stages of your business's working capital cycle. This is where your payment terms, financing repayments and investment decisions will have significant impact on your business's cash flow and available working capital.

View the sample debtors and creditors analysis table to see the impact of debtors and creditors on your cash flow.

Calculate your business's ability to pay off short-term liabilities with current assets by using the current ratio (also known as working capital ratio).

Calculate current ratio

Invoices

An invoice is a record of purchase that allows your customers to pay you for the goods or services you've provided. Your invoices should include:

- type of product or service provided

- quantity of items purchased

- agreed price

- date of sale.

There are different types of invoices, so make sure you're using the correct type for your needs. Correct invoicing helps protect your business's cash flow, maintain good records and meet your tax obligations.

Make sure you handle any customer invoice queries quickly and fairly.

Regular invoices

Regular invoices are used by businesses that aren't registered for goods and services tax (GST). This means your invoices will not include a tax component. Do not use the term 'tax invoice' on these invoices.

Tax invoices

Use a tax invoice if your business is registered for GST. Tax invoices must include the GST amount for each item sold. You must provide a tax invoice if any of these circumstances apply:

- the purchase is taxable

- the purchase is more than $82.50 (including GST)

- your customer asks for a tax invoice.

The Australian Taxation Office provides free, online courses in tax essentials for small business owners, including working with GST.

If your customer asks for a tax invoice and you're not registered for GST, you should add a statement that no GST is applicable (e.g. add 'Price does not include GST' or 'Note: The GST sum is nil' on the statement).

Invoice tips

- Make sure you have your customer's correct details (e.g. address, phone number, email) to ensure invoices reach them promptly.

- Include your business details, including contact details—name, address, phone, email and Australian Business Number (ABN).

- Clearly outline the due date, payment terms and accepted payment methods.

- Include customer reference or order numbers associated with the sale.

- Follow up with your customers after sending an invoice to avoid payment delays and customer disputes.

- Issue your invoices promptly after a sale.

What to include on tax invoices

-

A tax invoice for sales of less than $1,000 (including GST) must include the following 6 pieces of information.

- The words 'Tax invoice' – preferably placed at the top of the invoice.

- Your identity as the seller (i.e. your business name or company name) – contact details are optional, but recommended.

- Your Australian Business Number (ABN).

- The invoice issue date.

- A brief description or list of the items or services sold, including quantity and price.

- The GST amount payable (if any). You should display the GST amount for each item separately, or, if the GST amount is exactly one-eleventh of the total price, you can use a statement such as 'Total price includes GST'.

There may be more requirements, depending on the total sale price and how you sell the goods or services.

-

Your tax invoice must include the following 7 pieces of information.

- The words 'Tax invoice' – preferably placed at the top of the invoice.

- Your identity as the seller (i.e. your business name or company name) – contact details are optional, but recommended.

- Your Australian Business Number (ABN).

- The invoice issue date.

- A brief description or list of the items or services sold, including quantity and price.

- The GST amount payable (if any). You should display the GST amount for each item separately, or, if the GST amount is exactly one-eleventh of the total price, you can use a statement such as 'Total price includes GST'.

and - The buyer's identity (i.e. business name, company name or ABN).

There may be more requirements, depending on the total sale price and how you sell the goods or services.

-

Make sure your invoice is accurate, easy to understand and includes:

- a summary of the total payment amount

- a due date

- how to pay the invoice

- clear description of goods or services provided

- information on how to arrange return of goods and services and credit notes

- details of any agreed discounts

- information about late payment penalties

- information about outstanding payments

- delivery charges, if applicable

- period of work the invoice refers to, if relevant

- contact phone number and email address for any queries (e.g. for non-delivered items).

Read more about setting up your business invoices from the Australian Taxation Office.

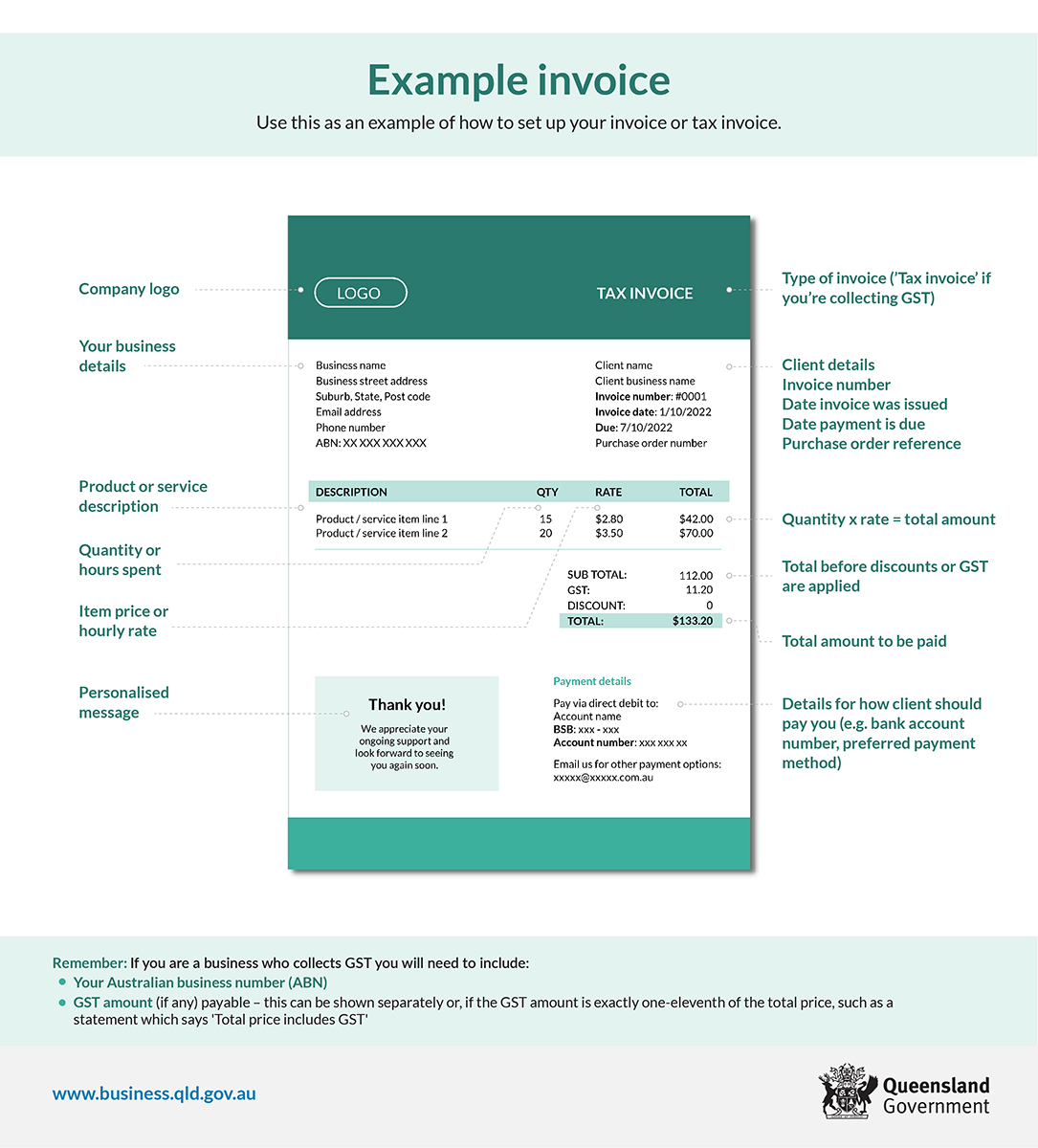

Example invoice

Use our invoicing infographic (JPG, 354KB) to learn how to set up your own invoice or tax invoice.

It shows:

- what information to include

- an example layout

- basic calculations.

Payment terms

Your business payment terms show when and how customers should pay you.

Your terms should make it as easy as possible for your customers to pay you promptly and efficiently. This will ensure you maintain good customer relationships and a healthy cash flow. If your terms make it difficult for customers to pay you easily, you risk:

- loss of income

- cash flow difficulties

- not being able to pay your suppliers on time

- additional business costs

- insolvency.

Developing payment terms

Payment terms usually include:

- a statement about your accepted payment methods

- availability and terms of credit

- debt collection policies

- terms and conditions that include the number of days until customer payment is required, and any late fees for overdue invoices.

Credit terms

You may choose to offer your customers the option of credit. Think of a customer credit purchase as a business debt. Learn more about offering credit to your customers.

Standard terms of credit can include:

- no credit terms provided

- 7 days to pay from receipt of original invoice

- 21 days to pay from receipt of original invoice

- 28 days to pay from receipt of original invoice.

Offering credit can increase your sales but also brings the risk of non-payments. Before you decide to offer credit options, review whether it suits the nature of your business and whether it's standard practice in your industry or among your competitors.

When setting your credit terms:

- display payment terms clearly on your invoices – decide if you will allow customers to pay part of their invoice before or during the service period

- determine types of payment (i.e. card, cash or other)

- establish your credit limits – this can protect you from customers going into too much credit and not being able to repay you

- decide if you will have an early payment scheme with discounts if customers pay early

- determine each customer's ability to repay the credit – use credit checks to reduce any risk and check if someone is bankrupt

- set your customers' terms shorter than suppliers' terms to avoid being out of pocket

- investigate the costs involved with a credit card and other electronic transactions – you may need to add a surcharge.

Credit and payment policies

Clear credit and payment policies provide clarity for both customers and your business and reduces misunderstandings which can lead to disputes.

Make sure all of your employees are aware of your business's credit and payment policies and are trained in how to use them.

Ensure your payment and credit policies, and related training material, include information on:

- payment methods that your business accepts – include your process for providing receipts for cash and credit card payments

- extended credit terms – include the process for completing customer credit checks in your payment and credit policy staff training

- process for debt collection – include the timing and communication method(s) for following up unpaid debts.

Managing debtors

Debtors are people or businesses who owe you money. Managing your debtors correctly will help you get paid faster and prevent bad debts.

Managing debtors (credit management) includes:

- collecting debts on time

- setting credit limits and payment terms

- processing credit applications and credit checks

- enforcing a clear credit policy

- considering whether you will take out debtor finance.

Develop clear debt collection policies and procedures for you and your staff to follow. These may include:

- when to send out requests for payment

- how to display payment terms

- when to phone debtors – for example, your debt collection policy could state that only the business owner or the finance team are authorised to follow up on unpaid invoices when they are 10 days overdue

- when you will ask debtors to pay by a certain date

- circumstances around negotiating payment plans

- when to ask for debt agreements in writing and what to ask for

- when to engage a debt collection agency.

You must keep records of your debtors to determine your actual income and expenses for the year for income tax purposes. There are also laws governing how you follow up debts with your customers.

Chasing late payments

Being consistent when chasing debtors will help you to recover debts while maintaining good customer relationships.

Contact customers quickly about overdue invoices. For example, if you offer payment terms of 28 days, begin following up debtors when payments are 7 days overdue.

When managing debtors, you should:

- chase debts on a regular basis

- make sure your collection process is professional and polite while being clear about your terms

- request payment in writing as a reminder or final notice

- offer payment plans for customers struggling to pay

- apply penalties for late payments, such as charges or accrued interest

- refuse to supply further goods or services until bills are paid.

Consider if you should have merchant facilities (if you don't already) such as mobile EFTPOS or credit card devices to make it easier to get paid as goods or services are delivered.

You may have other options available to you for chasing late payments, including:

- issuing a letter of demand or, if the customer is a registered company, a statutory demand after seeking advice from a legal adviser

- using mediation, debtor finance or debt collection services

- taking legal action (as a last resort only).

Learn more about debt collection options.

Debt collection laws

By law, there are things you can and can't do to encourage debtors to pay.

You can:

- contact them to request payment by letter, phone or in person

- consider negotiating a payment plan that is suitable for you and the customer

- stop working for or supplying more products to the debtor until the outstanding invoice is paid.

You cannot:

- make contact outside of normal business hours

- threaten, harass, or physically intimidate the debtor

- take or sell any of the debtor's property, unless you have a court order.

Managing suppliers (creditors)

Suppliers (also known as creditors) provide you with the goods or services you need to operate your business. Having good relationship with your suppliers can be mutually beneficial, especially if your business hits challenging times.

Negotiate supplier contracts

When you start working with a new supplier, clearly document your agreed terms in a contract signed and held by both parties. Make sure you negotiate contract conditions (such as delivery times and payment terms) that you both agree on.

At a minimum, the contract with your supplier should include:

- a clear description of the goods or services to be provided

- price and payment terms

- delivery terms

- warranty periods

- dispute resolution terms, including how you'll both manage issues like late payment, and replacement of faulty or poor-quality goods or services

- responsibility for insurance of goods, including when in transit

- termination and exclusion clauses between both parties.

Negotiate payment terms

When discussing payment terms with suppliers, you may ask them to consider:

- extending their payment days (e.g. from 30 days to 45) to help you better manage your cash flow (their terms may not allow this)

- quarterly payments, rather than monthly payments (e.g. utility and energy providers)

- starting the payment term from completion of delivery rather than beginning with milestone payments

- pricing options, such as lower prices on bulk or regular orders or discounts for on-time payment.

Review supplier payment terms regularly to help you manage your cash flow.

If you need to return goods:

- ensure the supplier provides a new invoice

- where an invoice is in dispute, do not process the payment until a credit note is provided.

Pay your suppliers regularly and on time

Try to pay your suppliers weekly or in periods that match typical account settlement periods (e.g. every 14, 21 or 28 days).

You may choose to pay invoices on their due date to maintain a positive cash flow position for your business. Avoid paying after the due date.

Set up payment systems to support your supplier payment policy. This will ensure you pay suppliers on or by the due date, avoid late payments and avoid duplicate payments.

Building relationships with suppliers

Strong relationships with suppliers can play an important role in supporting your business.

Establish and maintain good long-term working relationships with your suppliers by:

- communicating regularly with your suppliers and discuss opportunities

- discussing issues or concerns in an open and constructive manner

- listening to the supplier's perspective

- communicating regularly on issues as they are identified

- keeping track of your supplier's performance

- agreeing on a standard ordering process

- paying your accounts on time.

Strong relationships with your suppliers can be especially important when your business is going through a challenging period. If you've proven to be a good customer, your supplier may be willing to help you out with increased payment terms, higher credit amounts or loyalty discounts.

Not meeting agreed terms with suppliers

There may be times you need to pay outside of your agreed payment terms. Having a good relationship with your suppliers can mean they are more willing to help you out during difficult times for your business.

Contact your supplier as soon as you know you won't be able to meet the agreed terms. Discuss your concerns openly and honestly, and offer alternatives for when you will be able to meet terms again.

Be aware that if you're late on payment, suppliers can take back goods that you haven't paid for.

Your supplier may be able to reclaim unpaid goods if they've registered with the Personal Property Security Register (PPSR). The PPSR is an Australian Government register where suppliers can register their interest in personal property and have protection over those assets until they are fully paid.

Read more about managing late payments to suppliers.

Finding and choosing suppliers

Read about finding and choosing suppliers and maintaining supplier relationships.

Also consider...

- Learn more about resolving disputes with other businesses.

- Find out about negotiating successfully.

- Find out about record keeping for business.

- Learn more about stock control.

- Learn more about debt collection guidelines for collectors and creditors.

- Find information, tips and resources on setting up and managing your business finances from our Mentoring for Growth mentors.